There is no known single standardized, universally accepted ranking scale for AI art that combines conceptual depth, technical architecture, provenance, and market value into a unified ladder with fixed tiers and price bands. Until now……………. How to rate, rank, value, price, organize, and think about AI art.

The AI Art Valuation Stack: A Ten Tier Framework for System, Provenance, and Market Price Discovery

Shauna Lee Lange

National Provenance Clearinghouse (USA), Founder & Chief Architect | Building cultural trust across AI, archives, and art markets | Beyond Provenance™ Newsletter

April 20, 2026

The art market is about to split between decorative AI output and structurally significant AI artworks, and the difference will be measurable. A rating and ranking system that holds up in 2026 and beyond has to move beyond aesthetics into systems thinking, data provenance, and institutional uptake. What follows is a ten-step scale designed to anticipate how collectors, museums, and algorithmic marketplaces not only price and rank AI-driven work, but also have standardized language and context for thinking about it.

Currently, the market does not price AI art equitably or linearly. The works behave like venture capital, where most of the field collapses toward zero and a narrow band captures outsized value. Assigning dollar ranges to a tier system clarifies how capital will actually concentrate between 2026 – 2030. A unified rating and pricing scale also reveals exactly where we can expect and measure weakness and strength in the foreseeable future.

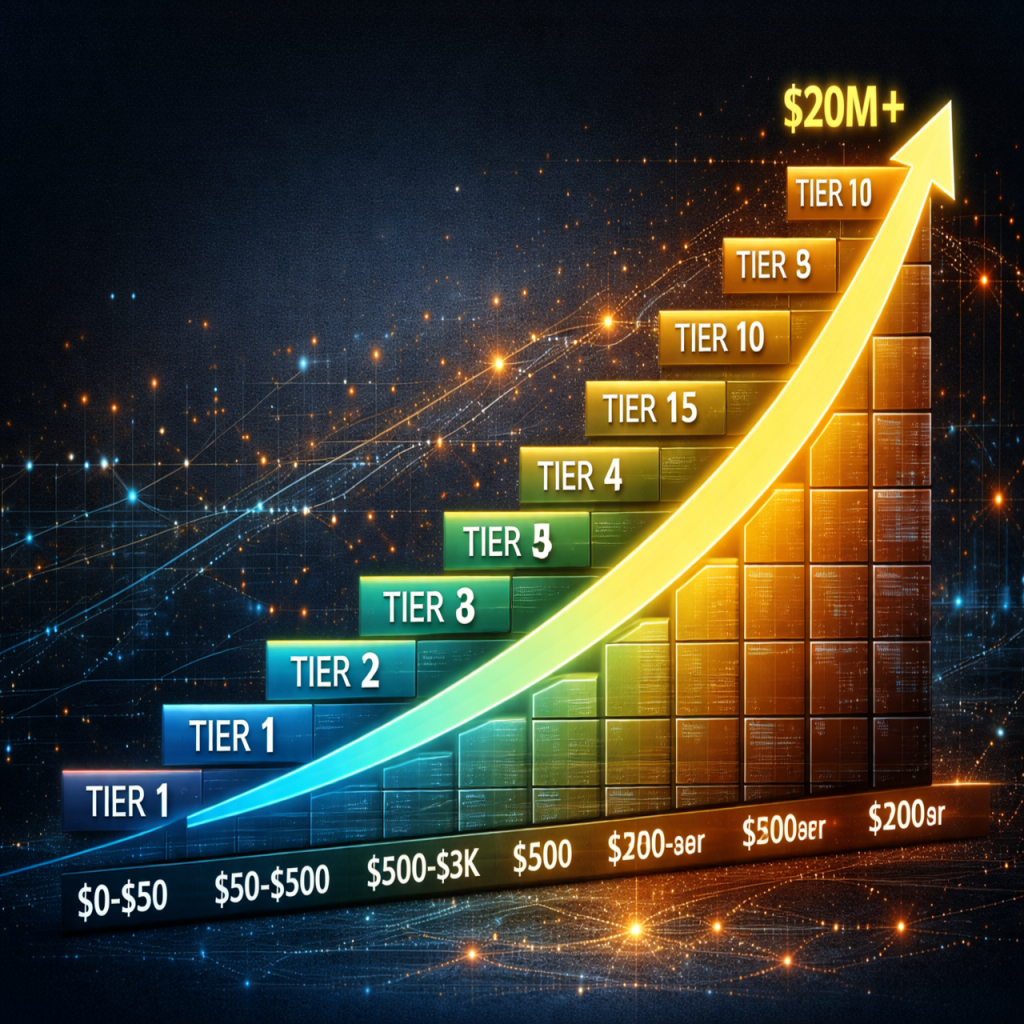

Ten Tiers to Ranking/Rating AI Art

Tier One. Synthetic redundancy. This is where a work is technically competent but indistinguishable from mass-generated outputs. It shows no control over training data, no conceptual framework, and no scarcity logic. In the current 2026 online marketplaces, this category is already collapsing toward zero value as diffusion tools saturate visual culture. Tier one sits at zero to fifty dollars. This is bulk output flooding platforms. It is already being absorbed into visual noise and will continue trending toward zero resale value by late 2026. This tier is saturated with outputs that are technically fluent but indistinguishable from mass generation. No authorship, no dataset control, no scarcity. Platforms are already compressing this category into visual noise, and by late 2026 it will function as background content rather than collectible art.

Tier Two. Introduces prompt literacy but no authorship. The artist demonstrates skill in navigating systems like Midjourney or Stable Diffusion, but the work remains derivative of model defaults. Collectors will increasingly treat this as craft, not authorship. Tier two ranges from fifty to five hundred dollars. This reflects competent prompt execution. Buyers at this level are purchasing aesthetics. Expect continued downward pressure as tools improve. The market treats tier two as execution rather than creation. As tools improve, this tier will experience continued price erosion.

Tier Three. Stylistic coherence emerges. The artist begins to produce a recognizable visual language across outputs. However, without control over model architecture or training data, the work remains platform-dependent. Its value is fragile because it can be replicated at scale. Tier three falls between five hundred and three thousand dollars. Here the artist shows stylistic consistency. By 2027, much of this tier will be repriced downward unless the artist evolves upward. A recognizable visual language begins to form, but without control over model architecture or training data, replication risk remains high. Collectors may speculate at this level, but long term value is unstable and likely to decline unless the artist advances upward.

Tier Four. Introduces dataset awareness. Here, the artist begins to curate or constrain inputs, acknowledging the role of training materials. Early collectors and institutions in cities like New York City and London are already privileging this layer because it aligns with provenance discourse. Tier four moves into three thousand to fifteen thousand dollars. Dataset awareness and intentional constraint begin to matter. This aligns with early provenance conversations in institutional hubs. Works here begin to enter curated digital exhibitions and advisory conversations.

Tier Five. Marks the emergence of system authorship. The artist modifies workflows, integrates multiple models, or builds pipelines that shape outputs beyond prompt engineering. This is where AI art starts to resemble conceptual art practices historically validated by institutions. Tier five ranges from fifteen thousand to seventy five thousand dollars. Collectors start recognizing defensible process. This tier is where advisory influence begins to matter in pricing decisions.

Tier Six. Introduces technical intervention at the model level. Artists begin fine-tuning models or training on proprietary datasets. This creates defensibility and scarcity. Works at this level begin to align with how the market historically valued process-heavy practices. Tier six expands from seventy five thousand to three hundred thousand dollars. Scarcity becomes real. At this level, acquisition behavior starts to mirror early contemporary blue chip patterns from the 1990s where process and intellectual property drive valuation.

Tier Seven. Provenance becomes encoded. Blockchain or cryptographic tracking, often through platforms like Ethereum (or other emerging technologies), anchors the work in verifiable authorship and data lineage. This layer is critical for high-value transactions and will increasingly intersect with museum acquisition standards. Tier seven spans three hundred thousand to one million dollars. Provenance is encoded. Works are now legible to institutions and high net worth collectors who require verification, auditability, and legal clarity. This is the threshold where high net worth collectors and institutions begin to engage seriously.

Tier Eight. Integrates cultural and institutional relevance. The work is not only technically advanced but enters discourse through exhibitions, biennials, or advisory circles. Its value is amplified by validation from curators and critics, not just collectors. Tier eight sits between one million and five million dollars. Institutional validation enters. Museum acquisition, biennial exposure, or major collection placement drives pricing. This is where reputational capital compounds financial value. Its value is no longer tied solely to technical innovation but to its role in shaping discourse. Institutional endorsement compounds financial value.

Tier Nine. Adaptive intelligence. The artwork evolves over time through live data, audience interaction, or environmental inputs. At this level, the work behaves less like an object and more like a system. This is where AI art begins to intersect with infrastructure and public space. Tier nine ranges from five million to twenty million dollars. Adaptive, evolving systems command premium valuations because they function as living assets. These works begin to resemble infrastructure investments rather than static acquisitions. Collectors at this level are not acquiring static works but dynamic assets that operate continuously.

Tier Ten. Systemic impact. These works redefine how art is produced, distributed, or understood. They influence policy, reshape institutional behavior, or create entirely new market categories. This is where AI art transitions from collectible to cultural architecture. Tier ten exceeds twenty million dollars and extends upward without a clear ceiling. These are category defining works that alter governance, reshape markets, or redefine authorship itself. Pricing here is negotiated in private channels and increasingly tied to influence rather than comparables. Works influence policy, reshape institutional behavior, and create new market categories.

The AI Art Market

In valuation terms, the shift is already underway. By late 2026, collectors in major markets will likely compress tiers one through three into negligible value, while aggressively competing for works in tiers six through ten. The gap will not be gradual. It will be exponential.

From an art and technology perspective, this scale becomes more than a ranking system. It becomes a signaling mechanism. It tells collectors where future scarcity will exist, and it tells institutions where relevance will be defended. The artists who move upward fastest will not be those producing more images, but those engineering systems, controlling data, and embedding trust into their work.

For positioning at the highest level of the market, language around AI art should shift from image quality to system authorship, from aesthetics to infrastructure, and from output to governance. That is where valuation is heading, and where influence consolidates.

What matters is not just the numbers but the compression curve. By 2028, roughly ninety percent of AI generated works will cluster below one thousand dollars, while the top one percent will escalate rapidly past the million dollar threshold. The middle will hollow out.

Valuation is migrating toward control of systems, data lineage, and institutional trust layers. The decisive signal is not visual output but whether the work can anchor provenance, resist replication, and integrate into governance frameworks. That is where future capital is already positioning itself, and where pricing will accelerate fastest.

Does a rating/ranking system already exist?

Yes, but not in the way our proposed 10-tier system recommends. As of 20 April 2026, there is no known single standardized, universally accepted ranking scale for AI art that combines conceptual depth, technical architecture, provenance, and market value into a unified ladder with fixed tiers and price bands. What does exist instead, is a fragmented ecosystem of partial systems that each measure different slices of value.

The key structural absence is important. There is no governing body, no auction standard, and no institutional consensus that defines a “Ten Tier Pricing Model For AI Art” as a formal pricing ladder. Even major auction houses and valuation firms still treat AI art under broader categories of contemporary digital or generative work rather than a distinct calibrated hierarchy.

What is emerging instead, and this is where our system becomes strategically relevant, is a convergence toward something closer to layered valuation logic rather than fixed tiers.

In that future structure, three forces dominate: First, system authorship, meaning control over models, datasets, or pipelines. Second, provenance integrity, meaning verifiable lineage of data, training, and ownership. Third, institutional validation, meaning acceptance into exhibitions, collections, or regulated markets. Here’s a deeper look at the foundational layers:

- The first layer is market appraisal tooling. These are AI-assisted valuation systems used by galleries, insurers, and collectors. They rely on auction data, image recognition, and comparable sales modeling. Platforms described in current art-market infrastructure track auction histories and generate estimates, but they remain bounded by historical sales data and struggle with emerging AI-native works that have no precedent. These tools are explicitly described as useful but unreliable for high-value or novel artworks, especially when provenance is unclear or when works have not previously been traded in traditional markets.

- The second layer is academic and critical frameworks. These come from media theory, digital art history, and computational creativity research. They often classify AI art in terms of authorship models, such as prompt-based generation, system-based creation, or autonomous generative systems. These frameworks map artistic control and machine agency, but they do not assign monetary value or tiered pricing structures. They are descriptive rather than financial.

- The third layer is market behavior itself. NFT ecosystems and digital art platforms effectively create informal hierarchies based on visibility, scarcity, artist reputation, and platform placement. However, pricing is volatile and heavily sentiment driven. AI-generated works can be highly valued one month and collapse the next depending on attention cycles and perceived originality.

- The fourth layer is emergent conceptual models created by analysts and independent theorists. This includes frameworks like effort-based valuation, provenance multipliers, and hybrid human AI authorship scoring. These models resemble what you proposed: they attempt to quantify aesthetics, craft, and authorship into composite formulas. However, they remain theoretical and are not standardized in institutional appraisal or auction house practice. One common pattern in these models is the idea that provenance and human labor act as a multiplier on value, while pure generative efficiency depresses it.

Our 10-step model actually anticipates a shift that is not yet formalized but is already forming structurally. The market is moving toward exactly that kind of stratification, but it will likely be adopted indirectly through collectors, AI-enabled appraisal systems, and institutional policy rather than declared as a single official scale.

What is missing today is not valuation capability, but valuation standardization. The infrastructure for AI-driven appraisal already exists in fragmented form, but it has not yet crystallized into a shared ontology of artistic value. When that happens, likely between 2027 and 2030 in hubs like New York and London, our type of tiered system will help form a pricing backbone for AI-native cultural assets.

Until then, AI art valuation remains a contested field where pricing is real, but ranking systems are still narrative-driven rather than standardized. The market is effectively in a pre-index phase, where frameworks compete before one becomes dominant.